Finance

QLCredit: The Complete Guide to Understanding Features, Benefits, and Responsible Credit Management

Managing your finances has become more important than ever, and digital credit platforms are changing how people access and manage borrowing. One name that frequently appears in online discussions is QLCredit. Whether you’re researching it for the first time or looking for a deeper understanding of its features, this guide explains everything you need to know.

In this comprehensive article, we’ll explore what QLCredit is, how it works, its potential benefits, possible limitations, eligibility considerations, application process, security practices, and tips for using any digital credit service responsibly.

By the end, you’ll have a clear understanding of whether QLCredit aligns with your financial needs and how to make informed borrowing decisions.

What Is QLCredit?

QLCredit is a digital credit platform designed to simplify access to financial services through an online application process. Like many modern lending platforms, it aims to reduce paperwork and provide users with a convenient way to apply for credit from their computer or mobile device.

Instead of relying entirely on traditional banking procedures, digital credit services typically use technology to streamline:

- Online applications

- Identity verification

- Credit assessment

- Approval notifications

- Account management

- Payment tracking

The exact products, eligibility requirements, and available services may vary depending on your location and applicable financial regulations.

Why Digital Credit Platforms Are Growing

The financial industry has rapidly adopted digital technologies. Consumers increasingly expect faster, simpler, and more transparent financial solutions.

Some of the major reasons include:

- Faster application processes

- Greater convenience

- Mobile accessibility

- Reduced paperwork

- Improved customer experience

- Digital document management

- Online account monitoring

These advantages have contributed to the popularity of services similar to QLCredit.

Key Features of QLCredit

Although features may differ depending on specific offerings, digital credit platforms commonly provide several valuable capabilities.

1. Online Application

Applicants can typically complete the process online without visiting a physical office.

This saves time while making financial services more accessible.

2. Digital Verification

Modern platforms often verify identity electronically using secure verification methods.

This helps reduce delays while improving security.

3. Account Dashboard

Many users appreciate having one place to manage their financial information.

Typical dashboard features include:

- Current balance

- Payment history

- Due dates

- Transaction records

- Account updates

4. Secure Data Protection

Financial platforms generally invest in security technologies such as:

- Encrypted connections

- Secure authentication

- Fraud monitoring

- Privacy protection

- Account verification procedures

5. Customer Support

Good customer support remains an essential feature of any financial platform.

Support may include:

- Email assistance

- Live chat

- Help centers

- Frequently asked questions

- Contact forms

How QLCredit Typically Works

Although every lender follows its own policies, the general process usually follows these steps.

| Step | Description |

|---|---|

| Create an Account | Register using personal information |

| Submit an Application | Complete the online application form |

| Identity Verification | Verify your identity through required documents |

| Review Process | The application undergoes evaluation |

| Decision | Approval or additional information request |

| Account Management | Monitor payments and account activity online |

This streamlined workflow helps reduce unnecessary delays while improving convenience.

Benefits of Using QLCredit

Many borrowers are attracted to digital credit services because of their flexibility and ease of use.

Some common advantages include:

Convenience

Applications can often be completed from anywhere with internet access.

Faster Processing

Digital systems help automate many administrative tasks.

Improved Transparency

Users can often review important information online, including:

- Payment schedules

- Outstanding balances

- Account activity

- Notifications

Better Accessibility

People living far from physical branches may appreciate online financial services.

Paperless Experience

Electronic documentation reduces paperwork while making records easier to organize.

Who Might Consider QLCredit?

Digital credit services may be useful for individuals who:

- Prefer online financial management

- Need convenient application options

- Want digital account access

- Value quick communication

- Appreciate electronic documentation

However, every financial decision should be based on personal circumstances rather than convenience alone.

Factors Lenders May Consider

Before approving credit, lenders commonly evaluate several factors.

Credit History

A positive borrowing history often improves approval chances.

Income Stability

Consistent income helps demonstrate repayment ability.

Existing Financial Obligations

Current debts may influence lending decisions.

Identity Verification

Applicants usually need valid identification.

Local Regulations

Requirements vary depending on applicable financial laws.

Tips for Improving Your Creditworthiness

Responsible financial habits can increase your chances of obtaining favorable lending terms.

Pay Bills on Time

Consistent payments help build a positive financial record.

Reduce Outstanding Debt

Keeping existing balances manageable improves your financial profile.

Monitor Your Credit

Review your financial information regularly for accuracy.

Avoid Excessive Borrowing

Only borrow what you genuinely need.

Maintain Stable Financial Records

Accurate income documentation can support future applications.

Responsible Borrowing Best Practices

Borrowing should always support your financial goals rather than create unnecessary financial pressure.

Follow these recommendations:

- Understand the repayment schedule.

- Read all terms carefully.

- Borrow only what you can comfortably repay.

- Keep emergency savings whenever possible.

- Track payment due dates.

- Contact customer support if financial difficulties arise.

- Avoid relying on multiple loans simultaneously.

These habits contribute to healthier long-term financial management.

Common Mistakes to Avoid

Many borrowers experience financial challenges because they overlook important details.

Avoid these common mistakes:

- Ignoring repayment deadlines

- Borrowing more than necessary

- Not reading the agreement

- Assuming approval is guaranteed

- Overlooking fees or applicable charges

- Sharing account credentials

- Failing to monitor account activity

Understanding Costs Before Applying

Before accepting any credit offer, carefully review all financial information.

Pay attention to:

| Important Factor | Why It Matters |

| Interest Rate | Determines borrowing cost |

| Repayment Period | Affects monthly payments |

| Processing Fees | May increase total cost |

| Late Payment Policies | Helps avoid penalties |

| Payment Methods | Ensures convenient repayment |

| Customer Support | Important if assistance is needed |

Understanding these details helps prevent unexpected financial obligations.

Security Tips When Using Digital Credit Services

Financial security should always remain a priority.

Here are several practical recommendations:

Use Strong Passwords

Create unique passwords that combine letters, numbers, and symbols.

Enable Two-Factor Authentication

If available, activate additional security measures.

Avoid Public Wi-Fi

Sensitive financial transactions should be completed over secure internet connections.

Monitor Your Account Regularly

Check for unauthorized activity.

Protect Personal Information

Never share sensitive financial details with unknown individuals.

How QLCredit Compares with Traditional Lending

| Feature | QLCredit-Style Digital Platform | Traditional Lending |

| Application | Online | Branch visit may be required |

| Documentation | Mostly digital | Often paper-based |

| Convenience | High | Moderate |

| Account Access | Online dashboard | Depends on institution |

| Communication | Digital | Phone, branch, or email |

| Processing | Often streamlined | May take longer |

Each option has advantages depending on individual financial needs.

Is QLCredit Right for You?

Choosing any credit provider requires careful evaluation.

Ask yourself these questions:

- Do I genuinely need to borrow money?

- Can I comfortably afford repayments?

- Have I compared available options?

- Do I fully understand the agreement?

- Have I reviewed all costs?

- Does this solution match my financial goals?

Taking time to answer these questions can help prevent unnecessary financial stress.

Practical Example

Imagine someone needs temporary financial assistance for an unexpected expense.

Instead of rushing into the first available offer, they should:

- Compare multiple credit options.

- Review repayment schedules.

- Understand total borrowing costs.

- Verify eligibility requirements.

- Read customer policies.

- Confirm they can comfortably make future payments.

This thoughtful approach often leads to better financial outcomes.

Future of Digital Credit Platforms

Financial technology continues evolving rapidly.

Emerging trends include:

- AI-assisted credit assessment

- Faster digital verification

- Improved fraud detection

- Personalized financial recommendations

- Enhanced mobile experiences

- Stronger cybersecurity measures

- Better customer education

As technology advances, consumers can expect digital lending services to become even more efficient while maintaining stronger security standards.

Frequently Asked Questions (FAQs)

What is QLCredit?

QLCredit is a digital credit platform designed to simplify online credit applications and account management through technology-based financial services.

Is QLCredit available everywhere?

Availability depends on geographic location, local regulations, and the provider’s supported regions.

How long does the application process take?

Processing times vary depending on verification requirements, submitted documentation, and internal review procedures.

Is my information secure?

Reputable financial platforms generally use encryption, secure authentication, and privacy safeguards to protect customer data. Users should also follow good online security practices.

Can I apply using a mobile device?

Many digital credit services are designed to work on smartphones, tablets, and desktop computers.

What should I check before accepting credit?

Review interest rates, repayment terms, fees, payment schedules, eligibility requirements, and the complete agreement before accepting any offer.

How can I improve my chances of approval?

Maintaining a positive credit history, stable income, accurate documentation, and responsible financial habits may strengthen your application.

Conclusion

QLCredit represents the growing shift toward digital financial services, offering a more convenient way for eligible users to manage credit online. Like any financial product, its value depends on understanding the terms, evaluating your financial situation, and borrowing responsibly.

Before applying, compare available options, review every detail of the agreement, and ensure the repayment schedule fits comfortably within your budget. Responsible borrowing is not just about getting approved—it’s about making financial decisions that support your long-term goals.

Ready to make smarter financial decisions? Continue exploring trusted financial guides on Rawqan to compare digital credit platforms, improve your financial knowledge, and choose borrowing solutions with confidence.

Finance

PO Box 55520 Portland Oregon Pay to the Order Of: Meaning, Purpose, and What You Need to Know

Introduction

If you recently received a document, check, or financial notice mentioning po box 55520 portland oregon pay to the order of, you may be wondering what it means and whether any action is required.

Many people encounter this phrase when receiving checks, settlement payments, refunds, rebates, or official financial correspondence. While the wording may seem confusing at first, understanding the purpose behind it can help you verify the legitimacy of a payment and avoid common financial mistakes.

In this guide, we’ll explain what “Pay to the Order Of” means, why a Portland, Oregon PO Box might appear on financial documents, how check payments work, and what steps you should take when you receive one.

What Does “Pay to the Order Of” Mean?

The phrase “Pay to the Order Of” is one of the most common terms found on checks.

It identifies the individual or organization authorized to receive and deposit the payment.

Simple Definition

“Pay to the Order Of” refers to the payee—the person, business, or entity that can legally cash or deposit the check.

For example:

- Pay to the Order Of: John Smith

- Amount: $500

In this situation, John Smith is the intended recipient of the funds.

Why This Phrase Matters

Banks use this section to determine:

- Who owns the payment

- Who can deposit the funds

- Whether the check is valid

- Whether endorsement requirements are met

Without a properly designated payee, a check may be rejected or delayed.

Why Does PO Box 55520 Portland Oregon Appear on Documents?

Many financial institutions, payment processors, claims administrators, and settlement services use centralized mailing centers.

A PO Box address often serves as:

- A payment processing center

- A customer correspondence location

- A return mail address

- A settlement administration office

- A refund distribution center

When people search for po box 55520 portland oregon pay to the order of, they are usually trying to identify the source of a mailed payment or verify whether a document is legitimate.

Common Reasons This Address Appears

| Mailing Purpose | Typical Use |

|---|---|

| Refund Checks | Tax, utility, or service refunds |

| Settlement Payments | Legal settlements or claims |

| Insurance Payments | Claim reimbursements |

| Rebate Programs | Product or service rebates |

| Administrative Notices | Official financial correspondence |

The presence of a PO Box alone does not indicate fraud or legitimacy. Additional verification is always recommended.

Understanding How Check Payments Work

Before cashing or depositing any check, it’s important to understand the payment process.

Basic Check Workflow

- Issuer creates the check.

- Payee is identified.

- Check is mailed.

- Recipient deposits the check.

- Bank verifies funds.

- Payment clears.

Key Components of a Check

| Check Element | Purpose |

|---|---|

| Pay to the Order Of | Identifies the recipient |

| Amount Box | Shows payment amount |

| Signature Line | Authorizes payment |

| Check Number | Tracking reference |

| Routing Number | Identifies bank |

| Account Number | Links payment source |

These components help financial institutions process payments accurately and securely.

How to Verify a Check Received Through Mail

Receiving an unexpected check can be exciting, but verification should always come first.

Review the Sender Information

Check whether the document includes:

- Company name

- Customer support information

- Payment explanation

- Reference number

- Official website

Inspect the Check Carefully

Look for:

- Professional printing

- Accurate spelling

- Consistent formatting

- Valid banking information

- Clear signatures

Contact the Organization

If you’re unsure about the payment:

- Call the official customer service number

- Use verified contact information

- Confirm the payment details directly

Avoid relying solely on information printed in suspicious correspondence.

Is PO Box 55520 Portland Oregon Associated with Legitimate Payments?

In many situations, centralized PO Boxes are used by third-party administrators and payment processors that handle large volumes of financial correspondence.

Examples include:

- Class action settlements

- Insurance claims

- Corporate reimbursement programs

- Consumer refunds

- Financial service notifications

However, because mailing addresses can change over time, the safest approach is always independent verification.

Warning Signs to Watch For

Be cautious if you notice:

- Requests for upfront fees

- Pressure to act immediately

- Requests for personal banking credentials

- Poor grammar or spelling

- Unexpected payment offers

Legitimate organizations rarely ask recipients to pay money to access funds already owed to them.

Common Situations Where You Might Receive Such a Payment

Settlement Checks

Settlement administrators frequently distribute payments through mailing centers.

Recipients may receive compensation related to:

- Consumer claims

- Data breach settlements

- Product recalls

- Employment disputes

Insurance Reimbursements

Insurance companies often use third-party processors to issue payments.

These may include:

- Medical reimbursements

- Property claims

- Vehicle claims

- Life insurance benefits

Corporate Refunds

Businesses regularly issue:

- Service refunds

- Subscription reimbursements

- Billing adjustments

- Account credits

Government-Related Payments

Certain government-related programs may utilize contracted payment vendors for distribution.

Always verify the source before depositing funds.

Benefits and Risks of Mailed Check Payments

Pros and Cons

| Pros | Cons |

|---|---|

| Easy to receive | Mail delays possible |

| Physical payment record | Risk of lost mail |

| Widely accepted | Fraud attempts exist |

| No internet required | Processing time may vary |

| Useful for refunds | Verification required |

Understanding both sides helps recipients make informed decisions.

Best Practices When Handling Financial Mail

Proper handling reduces the risk of fraud and payment complications.

Follow These Best Practices

Verify Before Depositing

Confirm:

- Sender identity

- Payment purpose

- Amount accuracy

Keep Records

Save:

- Check copies

- Envelopes

- Payment notices

- Correspondence

Deposit Promptly

Many checks contain expiration dates.

Depositing quickly helps avoid reissuance delays.

Monitor Your Bank Account

After depositing:

- Confirm the funds clear

- Watch for reversals

- Keep transaction records

Common Mistakes People Make

Many recipients unknowingly create complications when processing mailed payments.

Mistake 1: Depositing Without Verification

Unexpected payments should always be verified first.

Mistake 2: Throwing Away Documentation

Supporting documents often explain the purpose of the payment.

Mistake 3: Sharing Sensitive Information

Never provide:

- Online banking passwords

- Full account credentials

- Social Security details unless verified

Mistake 4: Ignoring Deadlines

Some checks expire after a specific period.

Mistake 5: Assuming Every Mailed Check Is Fraudulent

Many legitimate organizations still distribute payments through traditional mail.

How to Determine Whether a Payment Is Legitimate

A quick verification framework can help.

Payment Verification Checklist

| Verification Step | Why It Matters |

|---|---|

| Identify Sender | Confirms payment source |

| Review Documentation | Explains payment purpose |

| Contact Organization | Independent confirmation |

| Check Banking Details | Validates payment instrument |

| Monitor Deposit Status | Ensures successful clearance |

Following these steps significantly reduces risk.

Frequently Asked Questions About PO Box 55520 Portland Oregon Pay to the Order Of

Can I deposit a check if I don’t recognize the sender?

You should first verify the sender and understand why the payment was issued before depositing the check.

Does a PO Box indicate fraud?

No. Many legitimate organizations use PO Boxes for payment processing and correspondence.

What does “Pay to the Order Of” mean on a check?

It identifies the person or organization authorized to receive the funds.

Should I contact my bank before depositing an unexpected check?

If you have concerns about authenticity, contacting your bank can be helpful.

Can a legitimate settlement payment come from a PO Box?

Yes. Settlement administrators often use centralized mailing addresses.

Conclusion

Understanding po box 55520 portland oregon pay to the order of can help eliminate confusion when receiving financial correspondence. The phrase “Pay to the Order Of” simply identifies the intended recipient of a payment, while the Portland PO Box may function as a mailing or processing center for various organizations.

Whenever you receive an unexpected check or financial notice, take time to verify the sender, review accompanying documentation, and confirm the legitimacy of the payment. Following basic verification practices can help protect your finances while ensuring you receive funds that may rightfully belong to you.

FAQs

1. What does PO Box 55520 Portland Oregon Pay to the Order Of mean?

It usually refers to a payment document or check that includes a Portland mailing address and identifies the authorized payee.

2. Is PO Box 55520 Portland Oregon a real mailing address?

It may be used by organizations for payment processing or correspondence. Verification with the sender is recommended.

3. Why did I receive a check from a Portland Oregon PO Box?

Possible reasons include refunds, settlements, insurance reimbursements, rebates, or administrative payments.

4. Is it safe to cash an unexpected check?

Only after confirming the sender and payment purpose through official channels.

5. How can I verify a mailed payment?

Review the documentation, contact the issuing organization, and confirm the details with your bank if necessary.

/ You May Also Read /

WalmartMoneyCard Mobile App: Complete Guide to Features, Benefits, and Smart Money Management

Finance

WalmartMoneyCard Mobile App: Complete Guide to Features, Benefits, and Smart Money Management

Introduction

The WalmartMoneyCard mobile app has become a popular financial management tool for people who want convenient access to their prepaid card accounts. With mobile banking becoming a daily necessity, users increasingly look for simple ways to track spending, monitor balances, pay bills, and manage money directly from their smartphones.

Whether you already have a Walmart MoneyCard or are considering getting one, understanding how the app works can help you maximize its benefits. From account monitoring to security features and budgeting tools, the app provides a range of capabilities designed to simplify financial management.

In this guide, you’ll learn everything about the WalmartMoneyCard mobile app, including its features, advantages, limitations, best practices, and tips for getting the most value from the platform.

What Is the WalmartMoneyCard Mobile App?

The WalmartMoneyCard mobile app is the official mobile application designed to help cardholders manage their Walmart MoneyCard accounts. It allows users to access account information, perform financial transactions, and monitor spending from virtually anywhere.

Key Functions of the App

The app serves as a digital control center for your prepaid card account. Users can:

- Check account balances

- View transaction history

- Deposit checks remotely

- Transfer funds

- Pay bills

- Receive account alerts

- Manage security settings

- Track spending activity

Why Many Users Prefer Mobile Access

Traditional banking often requires visiting a branch or logging into a desktop portal. Mobile apps provide immediate access to financial information, making it easier to stay informed about account activity throughout the day.

Main Features of the WalmartMoneyCard Mobile App

The app offers several features designed to improve financial convenience and control.

Real-Time Balance Monitoring

One of the most valuable functions is the ability to check account balances instantly. Users can see available funds without waiting for statements or visiting physical locations.

Transaction Tracking

The application records recent transactions, helping users monitor spending habits and identify purchases quickly.

Mobile Check Deposit

Users can deposit eligible checks directly through their smartphones by taking photos of the front and back of a check.

Bill Payment Services

Many users appreciate the ability to pay bills directly from the app, reducing the need for separate payment platforms.

Fund Transfers

The app supports transferring money between eligible accounts, helping users manage funds efficiently.

WalmartMoneyCard Mobile App Features at a Glance

| Feature | Benefit | User Value |

|---|---|---|

| Balance Monitoring | Instant account visibility | Better spending control |

| Mobile Check Deposit | Deposit from anywhere | Saves time |

| Transaction History | Spending transparency | Easier budgeting |

| Bill Pay | Convenient payments | Fewer missed due dates |

| Account Alerts | Real-time notifications | Increased awareness |

| Security Controls | Better account protection | Improved confidence |

Benefits of Using the WalmartMoneyCard Mobile App

The app offers several advantages that appeal to both occasional and frequent users.

Convenience

Managing finances from a smartphone eliminates many traditional banking hassles. Users can access their accounts at home, at work, or while traveling.

Improved Financial Awareness

Frequent balance checks and transaction monitoring help users stay informed about spending patterns.

Faster Money Management

Tasks that once required multiple steps can often be completed within minutes through the app.

Better Organization

Digital transaction records simplify tracking expenses and reviewing financial activity.

Enhanced Accessibility

The app provides access to financial tools around the clock, making it easier to manage money whenever needed.

How the WalmartMoneyCard Mobile App Supports Budgeting

Budgeting becomes easier when financial information is available in real time.

Spending Analysis

Users can review transaction histories to identify where money is being spent most frequently.

Monitoring Available Funds

Regular balance checks reduce the likelihood of overspending.

Tracking Recurring Expenses

Viewing recurring charges helps users understand monthly financial obligations.

Budgeting Workflow Example

| Step | Action | Result |

| Check Balance | Review available funds | Understand spending capacity |

| Review Transactions | Analyze recent purchases | Identify spending trends |

| Categorize Expenses | Group purchases by category | Improve budgeting accuracy |

| Set Spending Limits | Create personal targets | Encourage financial discipline |

| Monitor Weekly | Track progress regularly | Stay on budget |

Security Features Available in the App

Security remains a major concern for financial app users. The WalmartMoneyCard mobile app includes multiple protection features designed to help secure accounts.

Login Authentication

Secure login procedures help prevent unauthorized account access.

Account Alerts

Notifications can inform users about important account activity.

Transaction Monitoring

Regular activity updates help identify unusual transactions quickly.

Mobile Device Protection

Using smartphone security settings adds another layer of protection.

Best Practices for Using the WalmartMoneyCard Mobile App

To maximize benefits, users should follow several recommended practices.

Enable Notifications

Real-time alerts help users stay informed about account activity.

Use Strong Passwords

Create unique passwords that are difficult to guess.

Review Transactions Frequently

Regular monitoring can help identify errors or unauthorized activity sooner.

Keep the App Updated

Installing updates ensures access to the latest features and security improvements.

Secure Your Smartphone

Use screen locks, biometric authentication, and device security settings whenever available.

Best Practices Summary

| Best Practice | Why It Matters |

| Enable Alerts | Improves account awareness |

| Use Strong Passwords | Enhances security |

| Review Transactions | Detects issues early |

| Update App Regularly | Accesses latest protections |

| Secure Mobile Device | Reduces unauthorized access risk |

Pros and Cons of the WalmartMoneyCard Mobile App

Pros

- Easy account access

- Convenient balance monitoring

- Mobile check deposit functionality

- Real-time transaction tracking

- Bill payment capabilities

- Helpful account notifications

- User-friendly design

Cons

- Requires internet access

- Some features may vary by account type

- Mobile check deposits may require processing time

- Users must maintain device security

Common Mistakes Users Make

Many users fail to take full advantage of the app because of avoidable mistakes.

Ignoring Notifications

Account alerts often provide important financial information.

Not Reviewing Transactions

Waiting too long to check account activity can delay issue detection.

Using Weak Passwords

Simple passwords increase security risks.

Skipping App Updates

Outdated versions may miss performance improvements and security enhancements.

Sharing Login Information

Account credentials should never be shared with others.

Who Should Use the WalmartMoneyCard Mobile App?

The app can be beneficial for a variety of users.

Busy Professionals

People with limited time often appreciate quick mobile access to account information.

Budget-Conscious Individuals

Real-time financial tracking supports spending control.

Frequent Travelers

Mobile account management allows access from multiple locations.

Digital Banking Users

Anyone who prefers managing finances through a smartphone may find the app particularly useful.

Tips for Getting the Most Value from the App

To improve your overall experience:

- Check balances regularly.

- Enable transaction notifications.

- Monitor recurring expenses.

- Deposit checks using mobile tools when available.

- Review monthly spending patterns.

- Update account information promptly.

- Use security settings consistently.

Conclusion

The WalmartMoneyCard mobile app provides a practical and convenient solution for managing prepaid card finances from a smartphone. With features such as balance monitoring, transaction tracking, mobile check deposits, bill payments, and account alerts, users gain greater visibility and control over their money.

While no financial app is perfect, following security best practices and monitoring account activity regularly can help users maximize the benefits available through the platform. Whether your goal is better budgeting, improved convenience, or easier money management, the WalmartMoneyCard mobile app offers tools that can support everyday financial needs.

Frequently Asked Questions

1. What is the WalmartMoneyCard mobile app used for?

The app helps users manage their Walmart MoneyCard accounts, check balances, review transactions, pay bills, and perform various financial tasks.

2. Can I check my balance using the WalmartMoneyCard mobile app?

Yes. Users can view available account balances directly within the app.

3. Does the app allow mobile check deposits?

Yes. Eligible checks can typically be deposited using the mobile deposit feature.

4. Is the WalmartMoneyCard mobile app secure?

The app includes multiple security features, and users can enhance protection through strong passwords and device security settings.

5. Can I track spending through the app?

Yes. Transaction history and account activity records help users monitor spending patterns.

/ You May Also Read /

Bop444Money Explained: Your Ultimate Guide to Financial Freedom

Social Security Group 1 Direct Deposit: Payment Dates, Eligibility & How It Works

For many founders in Dubai, there is a specific, unsettling moment that occurs right around the time the business starts to “make it.” Your revenue is climbing, your team is expanding, and your calendar is full. Yet, when you look at your bank balance, something doesn’t add up. You’re making sales, but you aren’t seeing the liquidity. Or perhaps you’re facing a massive Corporate Tax bill you hadn’t fully reserved for.

This is the “financial breaking point.” It’s the moment you realize that while your bookkeeper is excellent at recording the past, they aren’t equipped to navigate your future.

As a Dubai SME, you eventually face a critical crossroads: Do you hire a full-time Chief Financial Officer (CFO) to sit in your office, or do you leverage specialized cfo accounting services on an outsourced, fractional basis? In a city where overhead costs can make or break a company, making the wrong choice here can lead to either a bloated payroll or a dangerous lack of strategic direction.

Why SMEs Reach a Financial Breaking Point?

Most Dubai businesses start with a simple setup: an outsourced bookkeeper or a junior accountant who handles VAT filings and basic reconciliations. This works during the “survival phase.” However, once you cross into the “scaling phase,” basic accounting is no longer enough.

You know you’ve reached the breaking point when:

- The Profit vs. Cash Mystery: Your P&L shows a healthy profit, but you’re constantly stressed about meeting payroll.

- Reactive Decision-Making: You make big hires or investments based on “gut feeling” rather than data-driven forecasts.

- Budgeting is Non-Existent: You operate without a 12-month roadmap, making it impossible to measure actual performance against a plan.

- Investor/Bank Readiness: You’re approached for a partnership or loan, but your financial records aren’t robust enough to pass a rigorous due diligence process.

At this stage, you don’t just need someone to record the numbers; you need someone to tell you what the numbers mean.

What a CFO Actually Does? (Clarifying the Role)

There is a common misconception in the UAE that a CFO is just a “senior accountant.” This couldn’t be further from the truth. If your accountant is the historian of your business, the CFO is the architect.

While an accountant focuses on accuracy and compliance, a CFO focuses on value and strategy. Their core responsibilities include:

- Financial Planning & Forecasting: Building complex models that predict where the business will be in 12, 24, or 36 months.

- Cash Flow Management: Optimizing working capital so you always have the liquidity to move fast.

- Risk Management: Navigating the complexities of UAE’s evolving regulatory landscape, from Corporate Tax to ESR (Economic Substance Regulations).

- Capital Structure: Advising on whether to take on debt, seek equity, or reinvest profits.

A CFO is a decision-making partner. They don’t just report that your margins are down; they identify that your logistics costs in the Jebel Ali Free Zone have spiked and provide a plan to renegotiate those contracts.

Outsourced CFO Explained (The Fractional Model)

An outsourced CFO (also known as a Fractional CFO) provides high-level financial leadership on a part-time or project basis. Through modern cfo accounting services, an SME gets access to the brainpower of a seasoned financial executive without the AED 60,000+ monthly price tag.

How does it work?

Typically, an outsourced CFO works with you for a set number of hours per week or days per month. They integrate with your existing accounting team, providing the “strategic layer” that is usually missing. They use cloud-based dashboards to provide real-time visibility, often attending board meetings or management huddles remotely or in person.

Typical Services:

- Developing long-term growth strategies.

- Setting up advanced KPI tracking.

- Creating “what-if” scenario planning (e.g., “What if we open a branch in Riyadh next year?”).

- Managing relationships with banks and investors.

Full-Time CFO Explained (The In-House Model)

A full-time CFO is a dedicated C-suite executive who is fully integrated into your daily operations. They are physically present, managing your finance team, and involved in every high-level meeting.

Key Features:

- Deep Integration: They understand the “culture” and the “unspoken” nuances of the business.

- Immediate Availability: They are there to put out fires the second they start.

- Team Leadership: They are responsible for the mentorship and management of your internal accounting department.

This model is traditional, but it comes with a significant “carrying cost” that can be heavy for a scaling SME.

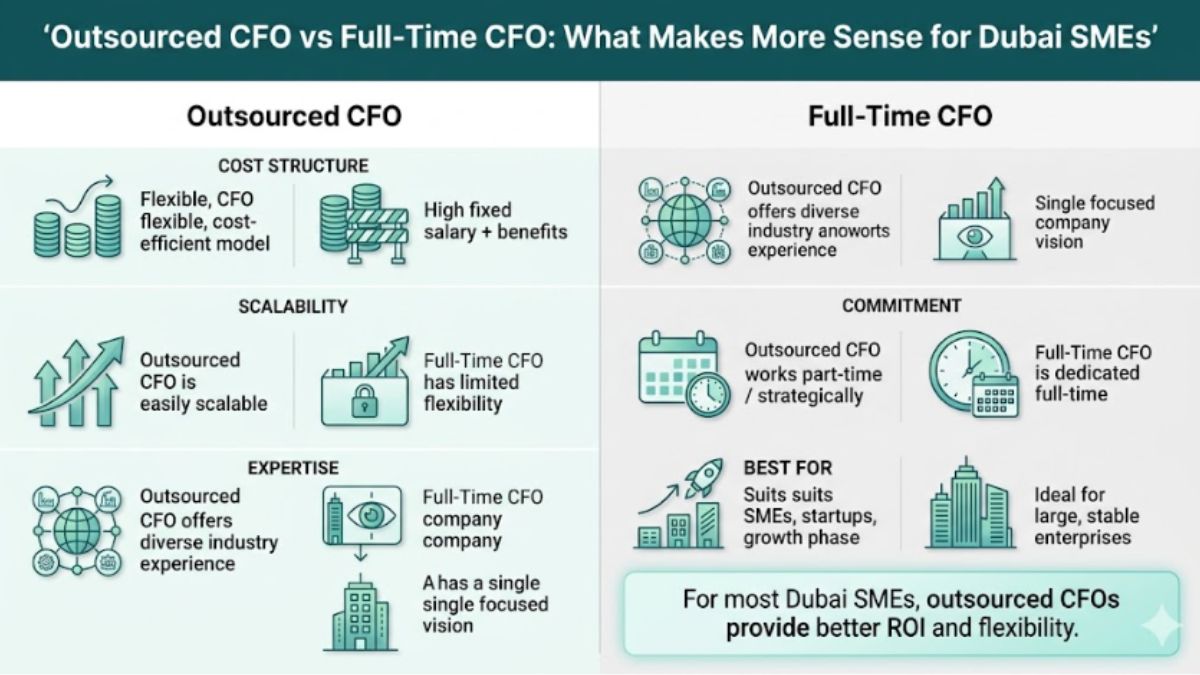

Direct Comparison: Outsourced vs. Full-Time CFO

| Feature | Outsourced CFO | Full-Time CFO |

| Cost | Flexible, retainer-based (Cost-effective) | High (Salary + Benefits + Visa + Bonus) |

| Flexibility | Scale up or down based on needs | Fixed long-term commitment |

| Expertise | Access to a firm’s collective knowledge | Limited to one individual’s experience |

| Onboarding | Rapid (Plug-and-play systems) | Slow (Recruitment and cultural integration) |

| Focus | Strategic outcomes and efficiency | Operational management and daily presence |

Cost Breakdown: Paying for Outcomes vs. Presence

In Dubai, the cost difference is staggering.

Full-Time CFO: A qualified CFO in the UAE can easily command a salary between AED 45,000 and AED 80,000 per month. But the “hidden costs” add at least 30% more:

- Employment visa and health insurance.

- Annual airfare allowances.

- Schooling allowances (common for senior roles).

- End-of-service gratuity.

- Recruitment fees (often 15-25% of annual salary).

Outsourced CFO: Specialized cfo accounting services typically operate on a monthly retainer that might range from AED 5,000 to AED 15,000, depending on the complexity of your business.

The ROI perspective is simple: For a scaling SME, is it better to pay AED 700,000 a year for someone to be “present,” or AED 120,000 a year for someone to deliver the exact same strategic outcomes?

When Does Each Option Make Sense?

Choose an Outsourced CFO if:

- You are a Scaling SME: You’ve outgrown your accountant but aren’t yet at AED 50M+ in revenue.

- You Need Strategy, Not Management: Your current accounting team is okay at data entry, but you need someone to help with the “big picture.”

- You are Fundraising: You need to get your “books in order” and build a valuation model for a Seed or Series A round.

- You Value Flexibility: You want to avoid the risk of a “bad hire” in a high-salary position.

Choose a Full-Time CFO if:

- Extreme Complexity: You manage dozens of entities across multiple countries with hundreds of employees.

- M&A Activity: You are constantly buying or selling companies and need 24/7 internal oversight.

- Revenue Scale: Your business generates enough cash flow that the AED 800k annual cost is a negligible percentage of your overhead.

UAE-Specific Considerations: Why Local Expertise Matters?

Dubai is a unique financial environment. You cannot use a “generic” CFO model from London or New York and expect it to work here without local calibration.

- Corporate Tax Impact: With the 9% Corporate Tax now a reality, SMEs need a CFO who understands the nuances of “Taxable Income” vs. “Accounting Profit.”

- VAT Compliance: HMRC-style audits are becoming more common in the UAE. An outsourced CFO ensures your systems are “audit-ready” at all times.

- Free Zone vs. Mainland: Navigating the financial implications of being in the DIFC versus a Mainland LLC requires specific local knowledge.

- The Dubai Speed: Business moves fast here. An outsourced model allows you to deploy expert financial leadership in days, whereas hiring a full-time CFO can take 4-6 months of recruitment.

Real Business Scenarios

Scenario A: The Tech Startup

A Dubai-based fintech startup just raised $2M. They need to show the board a clear “burn rate” and a path to profitability. A full-time CFO is too expensive and would eat their runway.

Solution: Cfo accounting services provide the “Board-Ready” reporting and investor relations support they need at a fraction of the cost.

Scenario B: The Established Trading Company

An SME in Al Quoz is struggling with cash flow. They have millions in stock but no cash to pay suppliers. Their accountant is overwhelmed.

Solution: An outsourced CFO steps in for 3 months to optimize inventory turnover and renegotiate credit terms with suppliers, instantly freeing up cash.

Common Misconceptions

- CFOs are only for big corporations.Actually, SMEs need them more because they have less room for financial error.

- Outsourced CFOs are less committed.Professional firms rely on results to keep their retainers. Their commitment is tied to your success, often more so than an employee waiting for their next paycheck.

- Accountants and CFOs do the same job.An accountant tells you where you’ve been; a CFO tells you where you’re going.

Hidden Risks of Choosing the Wrong Model

Choosing a full-time CFO too early is a “silent killer” of cash flow. We have seen SMEs hire a high-priced executive who spends 80% of their time doing “managerial” work that a junior accountant could do. This is a waste of capital.

Conversely, staying with only an accountant for too long leads to “Strategic Blindness.” You might miss a market shift or fail to realize you are selling a product at a loss until it’s too late to recover.

Transition Strategy: When to Move?

The transition doesn’t have to be all-or-nothing. Many successful Dubai SMEs use a Hybrid Model:

- Stage 1: Internal Bookkeeper + External CFO accounting services.

- Stage 2: Internal Finance Manager + External CFO for high-level strategy.

- Stage 3: (At significant scale) Full-time Internal CFO.

Knowing when to “upgrade” is a key part of the CFO’s job. A good outsourced CFO will be the first person to tell you, “You are now large enough that you need someone in-house full-time.”

How to Choose the Right CFO Support?

Before you make a hire, ask these four questions:

- What is the specific problem I’m trying to solve? (Is it daily team management or long-term growth strategy?)

- Does the person/firm have UAE-specific tax and regulatory experience?

- What is the Speed to Value? (How long will it take for them to impact my bottom line?)

- Is the cost sustainable? (Can we afford this if revenue dips for two months?)

Frequently Asked Questions

What is the core difference between an outsourced CFO and a full-time CFO?

A full-time CFO is a permanent employee managing your entire finance function daily. An outsourced CFO delivers the same senior-level strategy forecasting, investor reporting, cash flow management on a flexible, part-time basis. You get the expertise without the salary, visa, gratuity, and benefits of a permanent hire. For most Dubai SMEs, the outsourced model simply makes more financial sense.

How much does each option cost for a Dubai SME?

A full-time CFO in Dubai costs AED 45,000–85,000/month including salary, housing, insurance, and gratuity. An outsourced CFO typically runs AED 8,000–25,000/month with no hidden employment costs. For SMEs generating under AED 15 million annually, that saving is better reinvested into growth. The numbers strongly favour the outsourced model at this stage.

Does an outsourced CFO have the same expertise as a full-time one?

Often more. Outsourced CFOs work across multiple businesses simultaneously, giving them broader exposure to funding structures, market conditions, and financial challenges. A full-time CFO knows one business deeply but may have a narrower frame of reference. For Dubai SMEs, look for someone with UAE corporate tax, VAT, and GCC fundraising experience specifically.

When does a full-time CFO make more sense?

When your revenue exceeds AED 30–50 million, you manage a finance team of three or more, or you’ve closed a Series B with institutional investors demanding daily financial oversight. Below that threshold which describes most Dubai SMEs an outsourced CFO delivers better value at a fraction of the cost.

What tasks can an outsourced CFO handle for a Dubai SME?

Financial modelling, investor and board reporting, UAE corporate tax and VAT strategy, fundraising preparation, cash flow forecasting, and free zone versus Mainland structuring advice. They direct your existing accountant rather than replace them. It is a complete senior finance function without the full-time price tag.

How do UAE regulations strengthen the case for an outsourced CFO?

From 2023, UAE businesses must navigate 9% corporate tax, VAT, Economic Substance Regulations, and UBO disclosure requirements. An accountant alone cannot manage these strategically. An outsourced CFO with UAE-specific expertise ensures your SME stays compliant, avoids penalties, and is structured as tax-efficiently as possible.

Conclusion: Clarity Over Presence

In the competitive landscape of Dubai, the right choice isn’t about how many people are sitting in your office.it’s about the quality of the insights driving your decisions.

For the vast majority of SMEs in the UAE, the outsourced model offers the perfect balance of elite expertise and financial efficiency. By utilizing professional CFO accounting services, you gain the clarity of a veteran finance chief while keeping your capital where it belongs: invested in your growth.

That’s exactly where Dubai Business and Tax Advisors comes in. As a trusted financial partner across the UAE, they bring together seasoned CFOs, tax specialists, and accounting professionals who understand the region’s unique regulatory and commercial landscape. From VAT compliance to growth planning, they deliver real financial leadership without the overhead of a full-time hire turning your numbers into a clear roadmap for success.

Don’t let your business grow blindly. Whether you choose to hire in-house or outsource, ensure your financial leadership is looking through the windshield, not just the rearview mirror. With Dubai Business and Tax Advisors by your side, you’ll always have the clarity and confidence to make the right move.

Ready to see what strategic financial leadership can do for your business? It’s time to move beyond basic accounting.

You May Also Read:

-

Business2 months ago

Business2 months agoImage Search Techniques: Smarter Ways to Find Accurate Visual Results Online

-

Health2 months ago

Health2 months agoPravi Celer: Benefits, Uses, and How to Add It to Your Daily Diet

-

Business2 months ago

Business2 months agoUnderstanding the Idaho Policy Institute Formal Eviction Rate 2020 Shoshone County: Housing Stability Insights

-

Technology2 months ago

Technology2 months agoMessagenal Explained: Features, Benefits, and How to Use It Effectively

-

Sports1 month ago

Sports1 month agoAC Milan vs SSC Bari Timeline: Complete History, Key Matches, and Rivalry Moments

-

Business3 months ago

Business3 months agoUnlocking Business Potential: How Pedrovazpaulo Operations Consulting Transforms Organizations

-

Business2 months ago

Business2 months agoKlar Partners Ltd / Oleter Group Platform Strategy: Building Scalable Digital Business Ecosystems

-

Technology4 months ago

Technology4 months agoTop Features of ProgramGeeks Social You Didn’t Know About